Posted some content on Substack.com which may certainly be of interest to those who have been following my blog.

Personal Blogs

The Ghent System, Trade Unions and the Welfare State

Sunday 12 July 2026 at 17:53

Visible to anyone in the world

Unemployment is Rising. But Why? and What Should the Chancellor Do?

Wednesday 12 November 2025 at 08:43

Visible to anyone in the world

Edited by Alfred Anate Bodurin Mayaki, Thursday 13 November 2025 at 13:22

Overview

We are reminded this morning by the mainstream media that the Office of National Statistics has published the beautifully annotated labor market report on UK unemployment figures, showing how the rate for unemployment has spiked.

Now, in the mainstream New Keynesian DSGE model, unemployment is very nuanced. Why would I use this exact word? Well, because there are several ways of perceiving how economic factors can control firm-wide behaviour, where less endowed firms respond to higher inflation and higher wage demands. I would argue the UK is a very good example of how real rigidities permeate the economy because of the impromptu nature of central government actions taken to boost tax receipts, such as hikes in employer national insurance contributions.

UK Unemployment - The OBR's Onus

It is not rocket science and it is really not as it seems or as many would have you believe. ONS figures are not reflective of personal circumstance. Far from it. When, at any one time, unemployment rises to meet the effects of inflation expectations and firm de-hiring/separation decisions, this happens to new workers. The accusation of laziness or idleness as a reason is therefore not suitable to describe the effect in the data. Furthermore, if we examine the ONS data closely, we may find that the proportion of workers who are captured by long-term unemployment is lower than that of those who have been active in the most recent past. I am 95% certain of this.

Odd Levers and Some Proverbial Economic Analysis

We are led to believe the New Keynesian Phillips Curve has expired as a means of analysing inflation and unemployment dynamics. Influential actors close to the BoE, who are effectively authorities, such as Andy Haldane and Dave Ramsden, after him, have each mentioned this. But I don't bring up the subject because it's empirically fictional, or because the data seems to reject its assumptions, I bring up the subject because it's very, as I say, nuanced to view unemployment in isolation without critiquing the model of macroeconomic policy, which officials in His Majesty's Government and the country's independent central bank choose to advocate for. Side effects of medication often surface when a patient is recuperating from an illness, not during periods of relative good well-being.

It is therefore in the interests of the Office of Budget Responsibility's badged economists and civil servants acting as economic experts to view this eventuality as a phenomenon in an integrated, broader way, one which takes into account the UK's vacancy rate, its level of interest rates, and employer contributions. The idea that BOE's Governor Bailey has overcooked things by keeping rates on ice is one that I am fond of.

In my discussions about the Employment Rights Bill, I have always remained somewhat optimistic that reducing barriers towards entry to work (which is different from creating access for the unemployed) can be an action that reduces the economic implications of unemployment.

So Then, What Should the UK Chancellor Do Now?

Some argue there is very little that the Chancellor can do, when in fact there is plenty she may attempt to do. The proposed Autumn Budget (her second such attempt to re-balance government spending) will have limited economic effects; the Chancellor can, of course, choose to reduce national insurance contributions, propose to lower the commitment to uphold various taxes surrounding the operation of running a business, and to alleviate the cost of employment. This may work to increase the vacancy rate and therefore shift the future labor market employment level, but these may have very limited effects, especially against the headwinds of a relatively high level of interest rates, which hover at around 4% at the moment.

Just to put that in a geo-political context: The FTSE 100 is at an overwhelming 9,899.60 this morning, CPI was up 3.8% yoy in September, and West Texas Intermediate is currently 60.94 (Good economists may use the CPI/WTI spread and pass-through as an effective proxy for inflation dynamics and as a gauge for international economic shocks). Comparatively, the unemployment in Europe is 6.0% on average. Ahead of next year's 52nd G7 Leaders' Summit in France, where Finance Ministers will no doubt be gloating over their respective situations, you have to wonder whether a progressive policy on tax is still the right way to go for Chancellor Reeves.

Shameless Plug - Concurrent Research Projects +1

What else am I up to at the moment? Well, I am currently applying for doctoral studies, which I will be resuming sometime after completing the programme I am currently on at The Open University, and I am subsequently working on several concurrent independent projects, which have emerged as opportunities to enhance knowledge and research into public policy from a labor market perspective. All of my projects can be found in the links at the top of my OU Personal Blog.

The UK’s U/V - Beveridge curve charting observations where U=>1million

Friday 5 September 2025 at 17:34

Visible to anyone in the world

Edited by Alfred Anate Bodurin Mayaki, Friday 5 September 2025 at 19:43

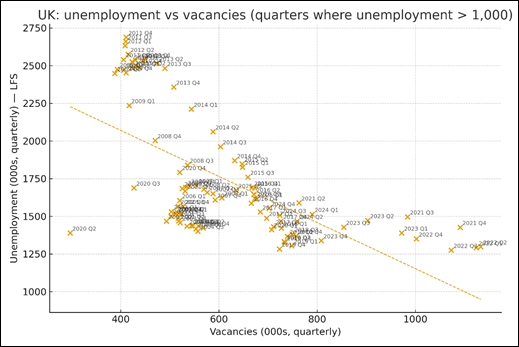

Fig 1: The UK’s U/V - Beveridge curve charting observations where U=>1million

Source:OpenAI ChatGPT (2025)

As I am currently working on an end-of-term assignment, I didn't realise that today’s nonfarm payrolls survey has been released, showing negative growth in job creation in key sectors of the US economy. Now, the above is a generative AI chart (above) illustrating a very profound relationship found in the literature; it projects the United Kingdom’s unemployment level by figure (>1million) and its vacancy rate expressed in hundreds of thousands, and noted in years and quarters. Can you spot the outlier?

As the plots on the chart show, when unemployment is high, vacancies are typically observed to be low (below 600,000), and vice versa. Except for a specific outlier (2020 Q2), which coincides with COVID-19, the U/V curve (also referred to as the Beveridge curve) is downward sloping (Pissarides, 2013: 292). In 2020 Q2, both unemployment and vacancies were low due to massive government job retention schemes that protected employment, combined with pandemic-related lockdowns that suppressed hiring activity and moved people into "economic inactivity". Despite a sharp drop in economic activity, the labor market was effectively frozen in place.

When inflation is high, this creates a further dilemma for businesses that post vacancies; the dilemma essentially is that unemployment tends to be low and when unemployment is low, the labour market is described as being ‘tight’ or there is a significant disparity between available vacancies and supply of workers seeking employment (assume these workers are structurally unemployed workers).

Now, although many overly-convoluted acronyms have been coined to describe aspects which the Beveridge curve reflects, that is, volatile and uncertain economics, acronyms such as VUCA and STEEPLE for example, there are still various reasons why approaching planned resourcing strategically can be beneficial for organizations.

Many strategic models outlined in my blog apply basic/hard forms of HRM, such as the Michigan or matching model authored by Fombrun, Devanna, and Tichy (1984). However, as one of my classmates who works in the UK Defence sector explained to me, organisations cannot ‘rest on laurels’ so to speak but should evolve through continuous adaptation to the challenge of new environments, such as during times of economic hardship.

References

Fombrun, C., Devanna, M. A., and Tichy, N. M. (1984). Strategic human resource management. New York, NY: John Wiley & Sons.

Pissarides, C.A. (2013) ‘Unemployment in the Great Recession’, Economica (London), 80(319), pp. 385–403

Congestion Externality in Search and Matching - A Theoretical Critique of Gertler-Trigari

Tuesday 18 June 2024 at 19:58

Visible to anyone in the world

Edited by Alfred Anate Bodurin Mayaki, Friday 21 June 2024 at 22:11

I'm thrilled to share that my review article is now available as an open-access resource, thanks to SSRN's esteemed repository. This milestone reflects the collaborative spirit of the academic community and the commitment to knowledge sharing.

The Open University Business School has been instrumental in this journey, fostering an environment where research and inquiry thrive. Thank you to Nicola Dowson from OU Library for your advice and guidance.

The main discussion related to the paper is based on this critique by a Warwick Economics Professor.

As I used a bootstrapped method and began with an identity that resembles the Pissarides/Mortensen matching function, some criticism of my paper I shall agree with concerns the relevance of the baseline 'Gertler-Trigari' model where 'congestion externality' creates some interesting rigidity.

The piece by Warwick Economics Dept's Professor, Thijs Van Rens argues there is zero 'congestion externality' in the identity I propose and in all 'GT' matching functions. I accept this claim. Most modern search and matching models operate with much of what he argues (the congestion rigidity created by firms competing for a narrow worker volume) as internalized components, usually referred to as rigidity or often as 'friction'.

The main discussion related to the paper is based on this critique by a Warwick Economics Professor.

As I used a bootstrapped method and began with an identity that resembles the Pissarides/Mortensen matching function, some criticism of my paper I shall agree with concerns the relevance of the baseline 'Gertler-Trigari' model where 'congestion externality' creates some interesting rigidity.

The piece by Warwick Economics Dept's Professor, Thijs Van Rens argues there is zero 'congestion externality' in the identity I propose and in all 'GT' matching functions. I accept this claim. Most modern search and matching models operate with much of what he argues (the congestion rigidity created by firms competing for a narrow worker volume) as internalized components, usually referred to as rigidity or often as 'friction'.

This blog might contain posts that are only visible to logged-in users, or where only logged-in users can comment. If you have an account on the system, please log in for full access.

Total visits to this blog: 231643